President Donald Trump answers questions from reporters during an event on protecting seniors with diabetes in the Rose Garden White House, Tuesday, May 26, 2020, in Washington. (AP Photo/Evan Vucci)

By Zeke Miller

President Donald Trump on Wednesday threatened social media companies with new regulations or even shuttering after Twitter added fact checks to two of his tweets.

The president can’t unilaterally regulate or close the companies, which would require action by Congress or the Federal Communications Commission. But that didn't stop Trump from angrily issuing strong warnings.

Claiming tech giants “silence conservative voices,” Trump tweeted early Wednesday, “We will strongly regulate, or close them down, before we can ever allow this to happen.” Later he tweeted without elaboration, “Big Action to follow.”

He repeated his unsubstantiated claim — which sparked his latest showdown with Silicon Valley — that expanding mail-in voting “would be a free for all on cheating, forgery and the theft of Ballots.”

There was no immediate reaction from Twitter or other social media companies to the president’s threats.

Trump and his campaign had lashed out Tuesday after Twitter added a warning phrase to two Trump tweets that called mail-in ballots “fraudulent” and predicted that “mail boxes will be robbed,” among other things. Under the tweets, there is now a link reading “Get the facts about mail-in ballots” that guides users to a Twitter “moments” page with fact checks and news stories about Trump’s unsubstantiated claims.

Trump replied on Twitter, accusing the platform of “interfering in the 2020 Presidential Election” and insisting that “as president, I will not allow this to happen.” His 2020 campaign manager, Brad Parscale, said Twitter’s “clear political bias” had led the campaign to pull “all our advertising from Twitter months ago.” Twitter has banned all political advertising since last November.

Trump did not explain his threat Wednesday, and the call to expand regulation appeared to fly in the face of long-held conservative principles on deregulation.

But some Trump allies, who have alleged bias on the part of tech companies, have questioned whether platforms like Twitter and Facebook should continue to enjoy liability protections as “platforms” under federal law — or be treated more like publishers, which can face lawsuits over content.

The protections have been credited with allowing the unfettered growth of the internet for more than two decades, but now some Trump allies are advocating that social media companies face more scrutiny.

“Big tech gets a huge handout from the federal government," Republican Sen. Josh Hawley told Fox News. “They get this special immunity, this special immunity from suits and from liability that’s worth billions of dollars to them every year. Why are they getting subsidized by federal taxpayers to censor conservatives, to censor people critical of China?”

There was no immediate reaction from Twitter or other social media companies to the president's threats.

Rent the Runway is making its trading debut on the NASDAQ. The fashion company has struggled since the onset of the pandemic, not having turned a profit since 2019. Crunchbase reporter Sophia Kunthara explains how Rent the Runway has had to make necessary changes to its business model in order to keep itself afloat.

As negotiations drag on in Washington, DC over President Biden's social spending bills, Senate Democrats have introduced a new idea to fund Biden's plans: taxing the unrealized capital gains held by billionaires. Barron's reporter Sabrina Escobar joins Cheddar News' Closing Bell, where she explains what's in the billionaire tax proposal, who it will impact, and why it's on the table.

GM exceeded earnings expectations, yet still felt the chip shortage squeeze. Baron's Senior Writer Al Root discussed GM's segue into the electric car car world despite its struggles.

Jay Jacobs, SVP and Head of Research & Strategy, at Global X ETFs, joins Cheddar News' Closing Bell, where he explains why the Dow and S&P fell from their recent records during Wednesday's session. Jacobs also broke down the numbers in Ford's Q3 earnings as the results rolled in.

Two recent studies by Conference Board, ESGauge, and Spencer Stuart find that the number of Black directors at S&P 500 companies is growing, but more needs to be done in order to see real gains in the boardroom. Jerusha Stewart, CEO of Take Your Seat joins Cheddar News to discuss what more needs to be done for a more inclusive workplace.

The freight industry has its newest unicorn. Flock Freight recently reached the $1 billion mark after recently raising $215 million dollars. It comes during a watershed moment for the global shipping and freight industry, with the pandemic and other issues leading to the ongoing supply chain crisis.

Flock Freight and its shared truckload service may be a solution. Flock Freight CEO Oren Zaslansky joined Cheddar News' Closing Bell to discuss.

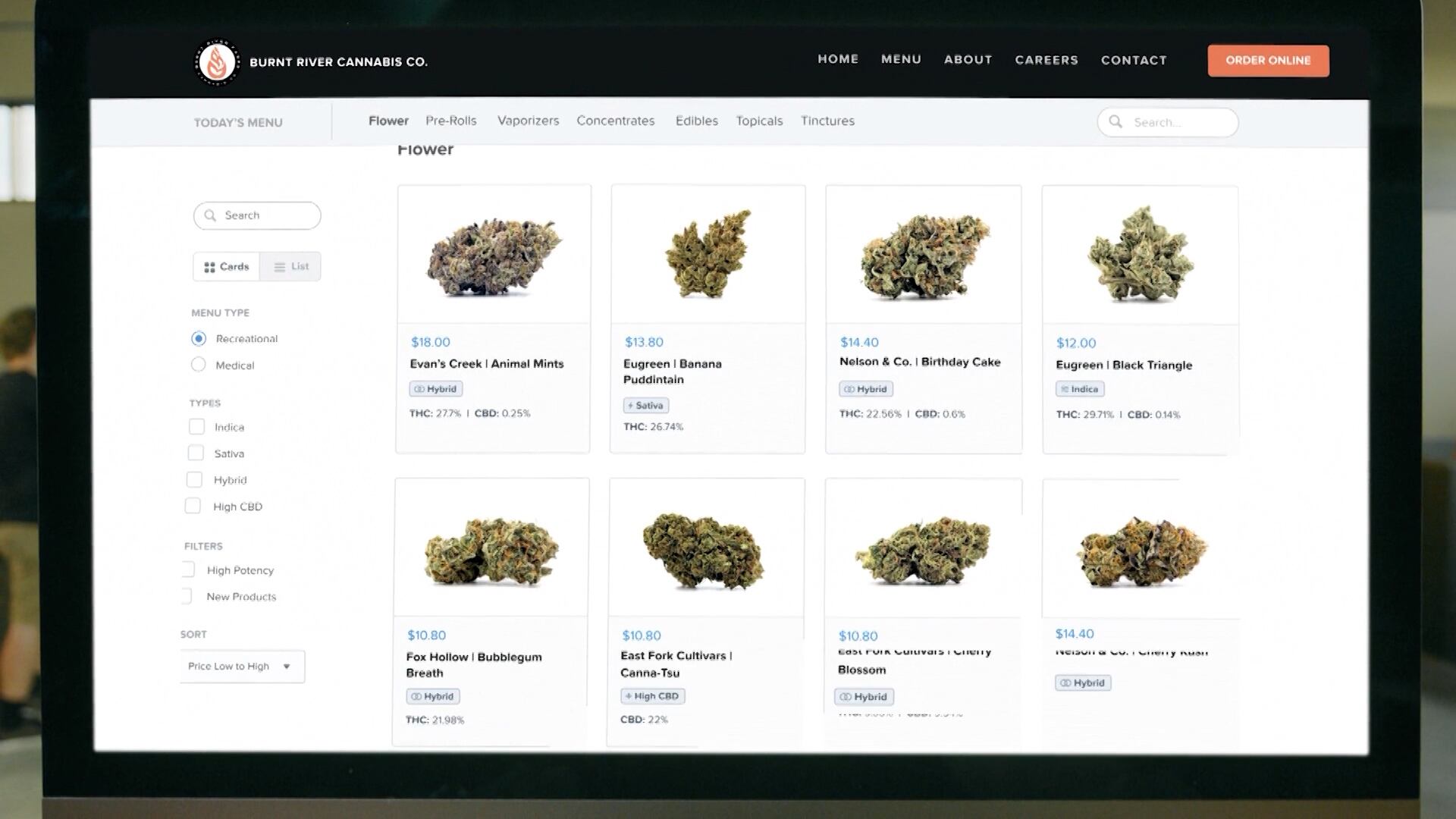

Cannabis tech company Dutchie raised $350 million in Series D Funding in October, and Ross Lipson, CEO and co-founder, joined Cheddar's "Closing Bell" to talk about how the funds will be used to grow the business. He noted that attracting the best talent, research and development, and expanding the brand's international reach are among the top priorities with this latest round of funding. Lipson also provided a breakdown of how his company "powers a dispensaries operations" through point of sales and e-commerce transactions.

Cloud data management company Informatica made its market debut on the New York Stock Exchange today under the ticker symbol INFA. Shares ending the day even after opening at $27.55. with shares priced at $29 apiece.

This is the second time the company has gone public after being founded back in 1993. Informatica then went private in a $5 billion deal in 2015. Now, the company is reentering public markets as a subscription business with a push to the cloud. Cheddar News welcomes CEO of Informatica, Amit Walia, to discuss.