Federal Reserve Board Chairman Jerome Powell testifies during a Senate Banking Committee hearing, Thursday Sept. 24, 2020 on Capitol Hill in Washington about the CARES Act and the economic effects of the coronavirus pandemic. (Drew Angerer/Pool via AP)

By Martin Crutsinger

The Federal Reserve kept its benchmark interest rate at a record low near zero Thursday and signaled its readiness to do more if needed to support an economy under threat from a worsening coronavirus pandemic.

The Fed announced no new actions after its latest policy meeting but left the door open to provide further assistance in the coming months. The central bank again pledged to use its "full range of tools to support the U.S. economy in this challenging time.” The economy in recent weeks has weakened after mounting a tentative recovery from the deep pandemic recession in early spring.

Several Fed officials have expressed concern that Congress has failed so far to provide further aid for struggling individuals and businesses. But the Fed's policy statement, issued after a two-day meeting, made no mention of lawmakers' failure to act.

A multi-trillion-dollar stimulus, enacted in the spring, had helped sustain jobless Americans and ailing businesses but has since expired. The failure of lawmakers to agree on any new rescue package has clouded the future for the unemployed, for small businesses, and for the economy as a whole. There is some hope, though, that a logjam can be broken and more economic relief can be enacted during a post-election “lame-duck” session of Congress between now and early January.

The central bank has been buying Treasury and mortgage bonds to hold down long-term borrowing rates to encourage spending. And it has kept its key short-term rate, which influences many corporate and individual loans, near zero. Some economists think the policymakers' next move will be to expand its bond buying effort, which is intended to boost the economy by lowering longer-term borrowing rates.

The Fed’s latest policy meeting coincided with an anxiety-ridden election week and an escalation of the virus across the country. Most economists warn that the economy cannot make a sustained recovery until the pandemic is brought under control and most Americans are confident enough to return to their normal habits of shopping, traveling, dining and congregating in groups.

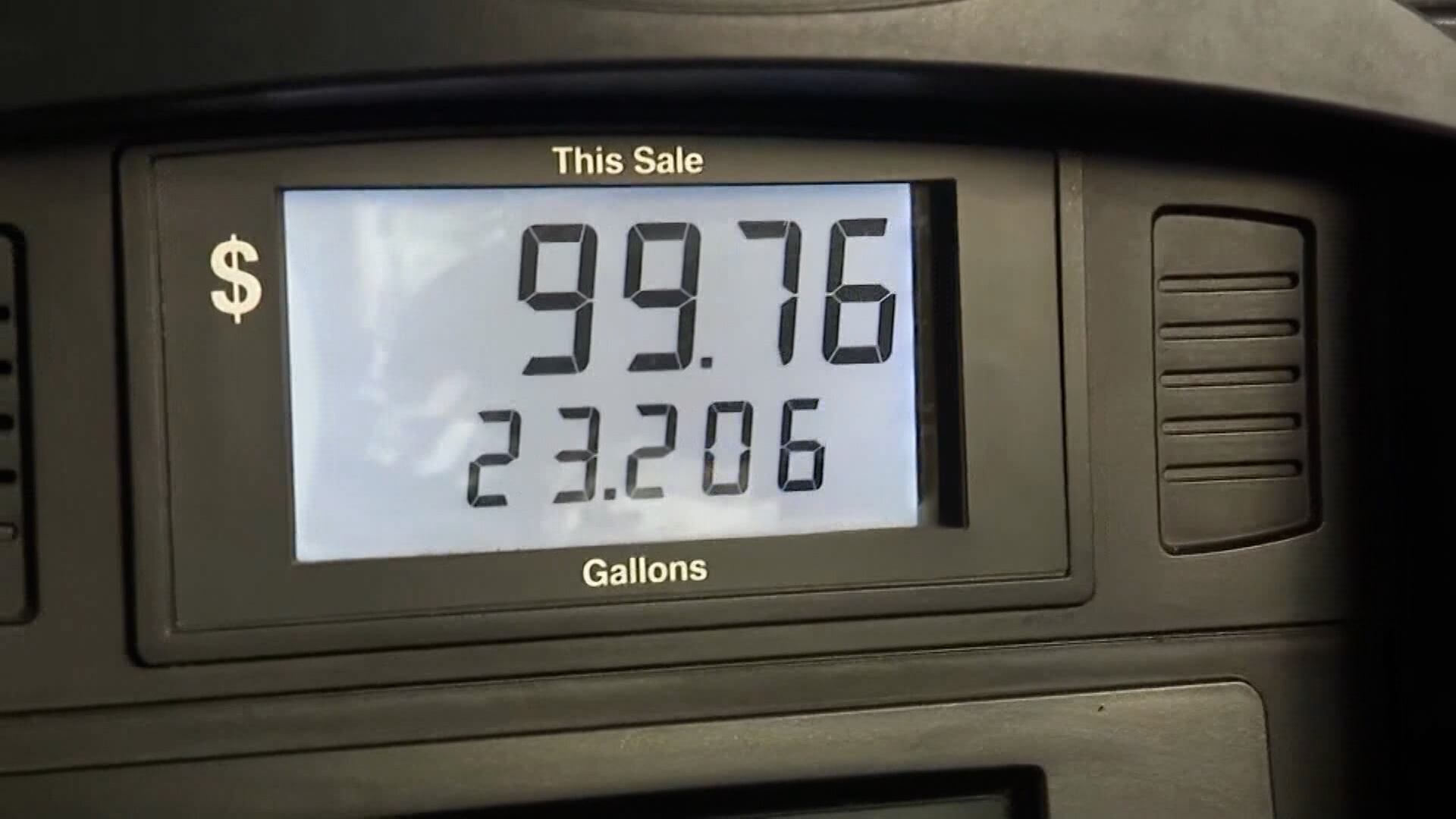

Fuel and oil prices have risen almost 17 percent since May, making the national gas prices reach nearly $5 a gallon. Andrew Lipow from consulting firm Lipow Oil Associates joined Cheddar News to discuss the future of gas prices. "The biggest issue on the oil market is really events that are beyond our control, which is what is happening over in Europe," he said, regarding the ongoing Russia Ukraine war. Lipow also said he predicted gas prices to hit $5.05 and that he's focused on the Biden administration's overtures in repairing a relationship with Saudi Arabia.

Target made some headlines this week as the retailer slashed its prices due to excess inventory. Cheddar News anchors Kristen Scholer and Ken Buffa break down Target as the Stock of the Week.

The electric vehicle maker filed a proposal for a three-for-one stock split, increasing the accessibility of shares for investors for a stock trading at around $700 a share. The move comes not long after tech giant Amazon announced a 20-for-one split. The number of authorized shares rises from two billion to six billion. It was also revealed that board member Larry Ellison does not intend to stand for reelection as it pertains to Tesla.

'Pride Portraits' is a trans-led organization aiming to visually represent the LGBTQ+ community one photograph at a time. Eden Rose Torres, founder and president of Pride Portraits, joins Cheddar News to discuss its participants and the issues the LGBTQ+ community still faces.

President Biden proposed a new rule that would add 500,000 chargers for electric vehicles nationwide. The proposal comes amid the rapid shift to EVs with dozens of automakers announcing plans for all-electric fleets within the next decade. But with the new surge will the U.S. have the proper infrastructure to keep up? Scott Painter, founder and CEO of Autonomy.com joined Cheddar's Opening Bell to discuss. "I really think the idea of standardization is a big deal. Standardization certainly makes it much better for everybody to be able to get a charge when they need one," he said.

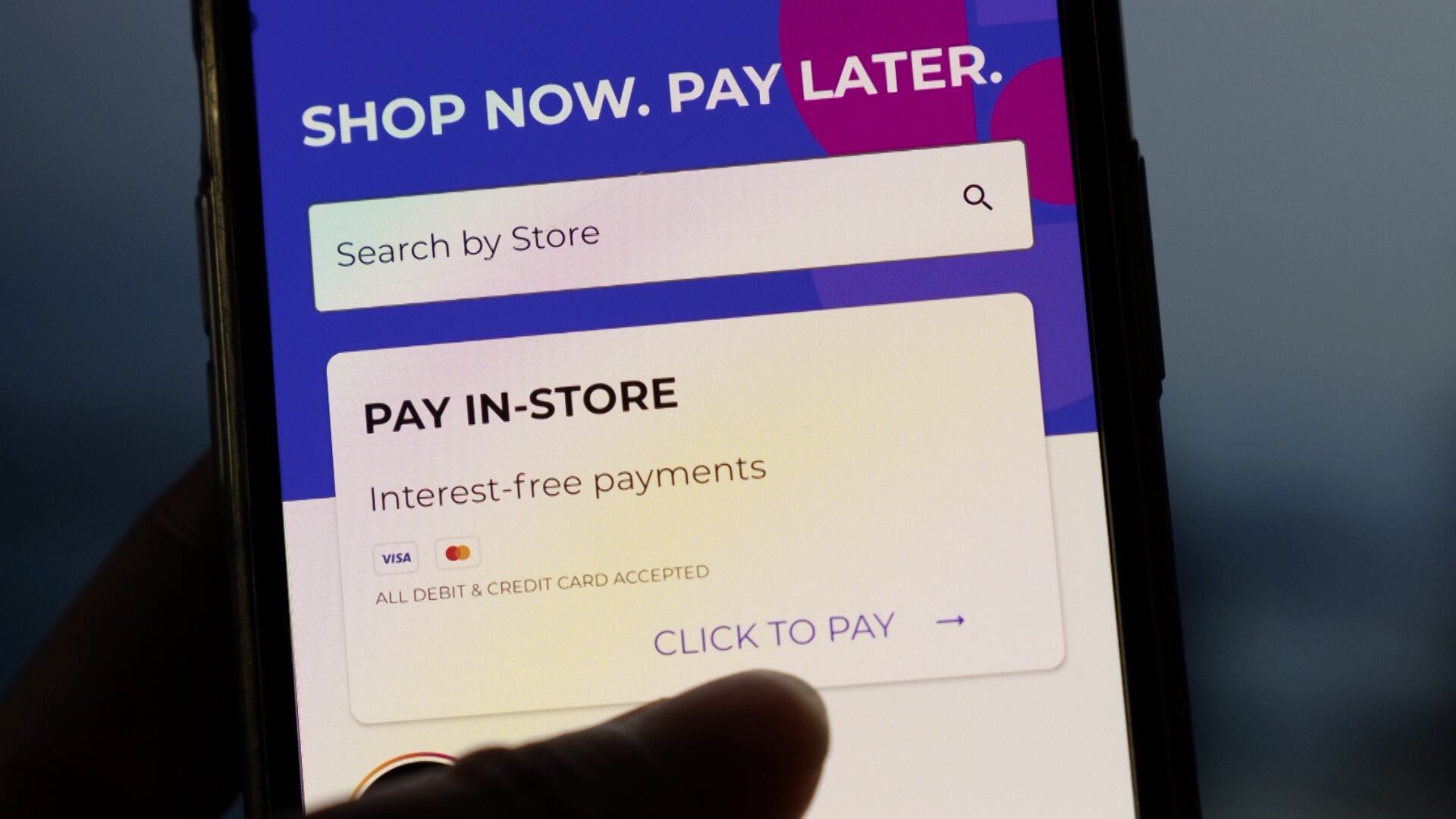

The Buy Now, Pay Later trend no longer has the luster it once had during the pandemic. Brandon Kreig, Stash CEO and co-founder, joins Cheddar News to give us insight on what happened and what's next for BNPL companies.

Join Cheddar News as we break down the top headlines this morning including updates on the Jan. 6 hears, the PGA suspension of 17 of the world's best golfers, and NASA's plans to study UFOs.